One of the confusing things about business insurance is jargon. It’s everywhere.

Take professional indemnity insurance (PI), for example. Or medical malpractice insurance. Among their many important features is the fact they're 'claims made' rather than claims-occurring policies.

Unfamiliar phrases, certainly. But to understand these words is to understand an essential part of your cover.

What does 'claims made' mean?

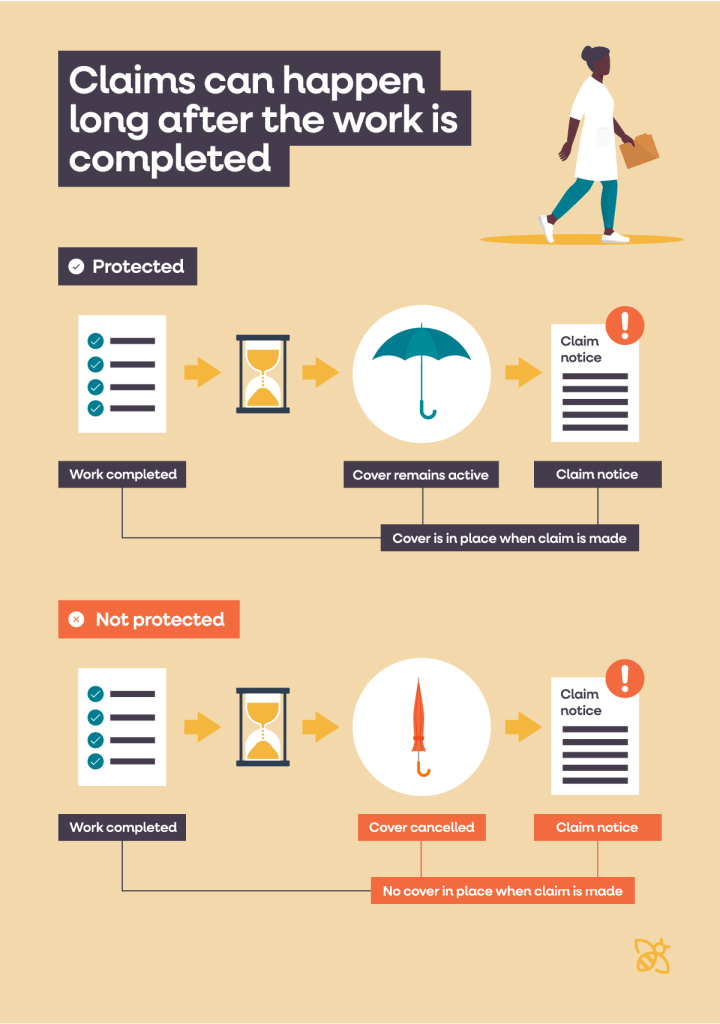

With a claims made policy, for a claim against you to be covered, your insurance has to be in force at two points:

- when you did the work, and

- when a claim about it is made.

Professional indemnity is mostly concerned with work you’ve already done, as that’s where the majority of claims come from. You can't be sued for a mistake you haven't made yet – and it can take months or even years for problems with your work to arise.

Similarly, medical malpractice (sometimes called ‘treatment liability’) insurance protects you when you’re carrying out a procedure or treatment and afterwards (assuming you keep your cover going). Considering that health-related problems can take a long time to surface, it’s a useful thing to have.

Which brings us to the really important bit: your ‘claims made’ insurance only covers you for as long as your policy is up and running. And that can create problems if you decide to cancel it later down the line...

Tell me more...

Let’s say you cancel your PI cover as soon as you finish a contract for a client. Or you stop offering a certain type of treatment and remove it from your malpractice policy straight away. Maybe you’ve stopped trading and/or retired completely.

If there’s a claim against you, say, two days or weeks after that, it won’t be covered – even if it relates to work you did when the policy was in place.

That’s an eyebrow-raiser for sure, and a common misunderstanding. It’s easy to assume that because you bought and paid for insurance at the time you did the work, any problems with it are covered even after you cancel the policy. That’s not the case, unfortunately...

So what's the answer?

If you want to make sure you’re still covered for your work after you’ve finished a job or carried out a treatment, there’s one obvious answer: you can keep your insurance running.

This is often a tricky one to weigh up – it could mean paying for cover for years after you’ve completed the work. Or stopped working altogether.

Another (and possibly cheaper) option is to add run-off cover to your policy. Put simply, it’s insurance that starts when you stop. You won’t be covered for any new work that comes in. But you’ll be able to fend off any potential claims from past clients.

How long you keep your run-off cover going after that is up to you. Though it’s worth noting that if you’re an accountant, architect, or a surveyor, your professional body may stipulate how many years you’d need run-off for. It’s always best to check with them before you make any decisions.

What's the difference between 'claims made' and 'claims occurring' insurance?

Public liability insurance and employers’ liability insurance are both claims-occurring policies and work somewhat differently from professional indemnity and medical malpractice insurance.

As with PI and medical malpractice, for a claim under one of these policies to be covered, the insurance has to be in force at the time of the incident. Simple enough.

However, it’s the insurer at the time of the incident that covers it, regardless of when the claim is made.

The obvious difference here is that, unlike claims made policies, claims-occurring policies still cover you even after you’ve switched your policy to another insurer. Or even if you’ve cancelled it altogether.

That isn’t the case with claims made policies. Making it essential to know exactly what kind of policy you have.

Jargon busted

So, there we go. That should have made things a little clearer for you. However, we haven’t covered everything to do with the nuts and bolts of keeping your cover going.

There’s retroactive cover, which stretches your cover back if run-off isn’t an option.

Or you can call us up on 0345 222 5391 with any questions. We’re always happy to clarify anything that might sound confusing.

Image used under license from iStock.

claimsinsurance explainedmedical malpracticeprofessional indemnity insuranceretroactive coverrun-off cover